The effects of a pension pause on young savers

Not contributing to a workplace pension for a prolonged period of time could lead to thousands of pounds in pension losses, Aegon has warned.

Employees aged between 22 and state pension age who earn over £10,000 per year, will automatically be enrolled into a workplace pension scheme, but they have the right to opt out. By doing so, they risk losing the valuable contributions from their employer (currently 3% on earnings above £6136) and the government who add a top-up to the employees payments.

Some may choose to opt out from the beginning but there are others who decide to take a break from contributing if their circumstances change after a few years of paying into a scheme. For those in their mid-20’s, financial pressures such as saving for a house deposit or clearing student debt may make opting out seem more appealing.

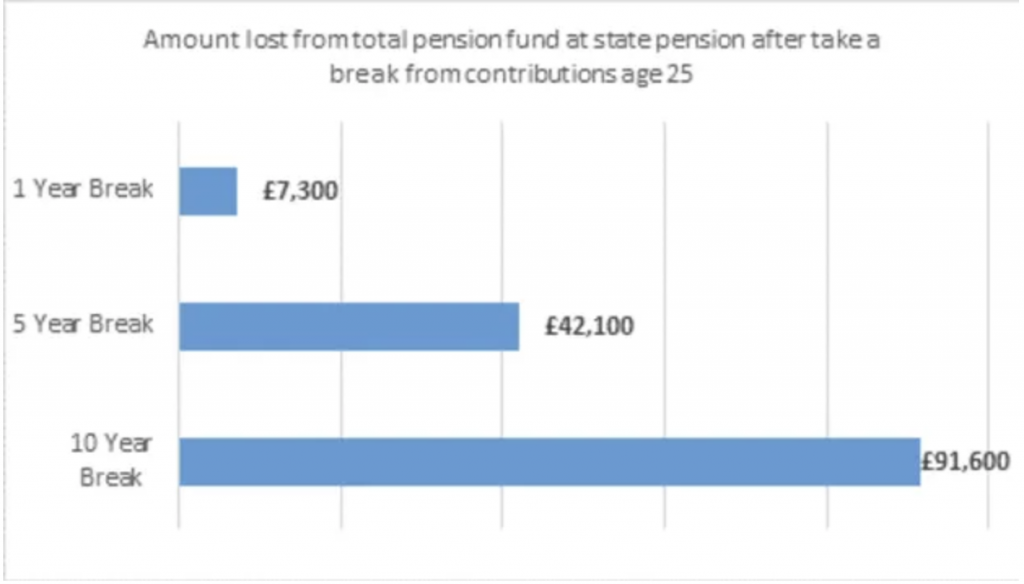

However, by taking a break, a 25-year-old graduate could miss out on £7,300 from their pension by the time they retire if they pause their payments for just 1 year. This would allow them to save just £622, according to research by Aegon.

For that same worker, a break of five years could see them lose £42,100 at state pension age and a ten year break could see then lose an astonishing £91,600. The full loss to the 25-year old will only be felt when the state pension kicks in, currently at age 68, as they lose out on the compound interest earned on their pension fund.

Competing demands for money short-term may mean saving for retirement decades into the future is pushed to the bottom of their financial concerns, however, “this should be avoided wherever possible” Steven Cameron, pensions director at Aegon comments.

The total value of that pension pot, without taking a break in contributions is calculated at £398,900 at state pension age.

It is really important to work with a specialist financial adviser who can help you reach your retirement goals.

Why not get in touch for a free no obligation consultation with us? letstalk@truwealth.co.uk

This analysis assumes a £20,000 starting salary at 22, increasing by 3.5% per year, investment growth of fund of 4.25% and retiring age of 68.